Conventional wisdom has been that cost of finding and extracting oil is on a secular rising trend. Given the current low price of oil, is that still credible?

A famous saying attributed to Keynes was his challenge to a critic: “When the facts change, I change my mind. What do you do, sir?” (1). In the global oil market, a key fact has changed. The price of a barrel of oil, which had been around $110 from 2010 to mid 2014, fell during the latter part of 2014 to around $50 and, if futures markets are to be believed, even by 2020 will still be below $70 (2).

Doesn’t this show that all that fuss about peak oil, scarcity and rising costs was wide of the mark? The function of prices, after all, is to allocate scarce resources: a fall in the price of a resource surely implies that it has become less scarce?

Let’s take this step by step. How will owners of operational oil wells respond to a reduction in price from $110 to $50? In most cases they will continue extracting oil at more or less the same rate, because their unit operating costs (including royalties where applicable) are generally below $50 (3,4). Oil production involves large exploration and construction costs, but once a well becomes operational these costs have already been incurred, so are irrelevant to the decision to continue production. A price of $50 may accelerate the closure of some ageing wells with high operating costs. The main impact of such a price, however, will be to discourage investment in new exploration and construction, bringing about a reduction in future oil supply. In summary, oil supply is price-inelastic in the short run, but price-elastic in the long run.

Similar considerations apply on the demand side. Car owners or those with oil-fired heating will increase their oil consumption only a little in response to even a large price reduction, because their consumption is largely determined by their needs and the particular vehicles or heating systems they have. Only when they come to buy a new car or boiler is a low price likely to have a major impact on their behaviour (making them less concerned about fuel-efficiency than they would be if the price were higher). Demand, too, is therefore price-inelastic in the short run, but price-elastic in the long run.

The price of oil at any time is determined by the equilibrium of short-run supply and demand. Why? Because in a largely free global market, buyers and sellers can rapidly exploit any mis-match between supply and demand. By so doing, they ensure that the price rapidly adjusts to restore equilibrium. Restoration of equilibrium requires changes in quantity supplied and/or demanded, and these are achieved within a timescale far too short for investment in new productive capacity or replacement of consumer durables to be of relevance.

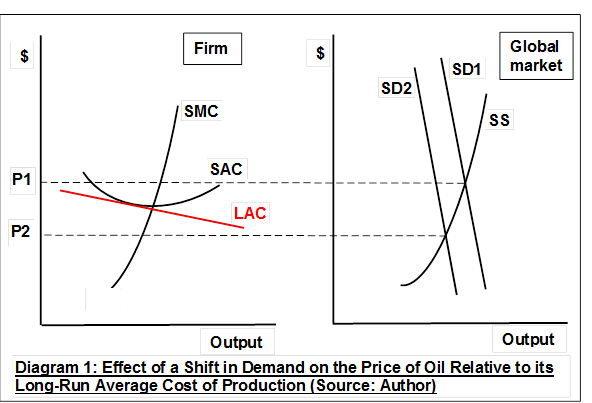

Diagram 1 below shows, on the left, the cost structure of a typical firm, and on the right, supply and demand in the global market (the output axis on the right is to a much smaller scale). The short-run average cost curve (SAC) shows the firm’s average costs given its current capital stock and rights to oil reserves, and from it is derived the short-run marginal cost curve (SMC), which is also its short-run supply curve. The sum of the short-run supply curves for all firms is the global short-run supply curve (SS), and this together with short-run demand determines the price of oil. Two not very different demand curves (SD1 and SD2) are shown, resulting, because of the inelasticity of both supply and demand, in very different prices P1 and P2. Similarly (not shown in the diagram) a small shift in the supply curve with constant demand can result in a large change in price.

Diagram 1 also shows the firm’s long-run average cost (LAC) curve, which assumes the optimum capital stock for each level of output. This is in red to highlight its importance: in the long run the firm can be profitable only if the price of oil generally exceeds average cost. Looking at it another way, the firm will not invest in exploration and construction unless it expects the future price of oil to exceed long-run average cost. The important point to note, as illustrated by P1 and P2, is that price at any time can be either much more or much less than long-run average cost.

A price well above or below long-run average cost can always be explained, with hindsight, in terms of past under- or over-investment. Investment in increased productive capacity tends to shift the global short-run supply curve to the right, reducing price. However, the forecasts of supply and demand on which firms base their investment plans may prove inaccurate for various reasons including new technologies, gamesmanship by major producers (eg OPEC), disruptions to supply, recessions and changes affecting competing energy sources. The relationship between the price of oil at any time and its long-run average cost of production is mediated by the productive capacity of the global oil industry, and for all these reasons it is difficult for the industry to get this right.

The price of oil at any time, therefore, tells us little about long-run average costs. The recent fall in price is quite consistent with a gradual increase in the cost of finding and extracting oil as the more accessible reserves are exhausted.

But is it actually the case that the long-run average cost of producing oil is rising, and likely to go on rising? To answer this, it helps to distinguish between conventional and unconventional oil, although definitions of these terms vary (5). Here I take conventional oil to be oil that can be extracted using traditional drilling methods from beneath land or shallow water. Such oil is becoming increasingly difficult to find (6). Even if it remains relatively cheap to extract where it can be found, its share of total oil production has declined, and is likely to decline further.

Unconventional oil – including tight oil (sometimes termed shale oil), oil sands and deep-water oil – contributed more than two-thirds of the increase in total oil production between 2000 and 2012 (7). Its share of total oil production will probably continue to increase as conventional oilfields are exhausted. Although each type of unconventional oil has its own characteristics, extraction costs are generally high, with break-even costs per barrel estimated at $65 for US tight oil, $75 for Canadian oil sands and $95 for deepwater oil (8).

In terms of long term trends in the oil market, the fall in price to $50 is just noise. The real signal is the effect it has had on firms’ investment plans. ExxonMobil is cutting its capital spending in 2015 by 12% (9), BP by about 20% (10), Conoco by 35% and Occidental by 33% (11). That is a strong indication that much previously planned investment would only be profitable at a price well above $50. That is what really does tell us something about average costs. So it remains highly credible that the cost of producing oil is continuing on an upward trend.

Notes and References

- Quite possibly a mis-attribution. See http://quoteinvestigator.com/2011/07/22/keynes-change-mind/

- CME Group: Crude Oil Futures Quotes http://www.cmegroup.com/trading/energy/crude-oil/light-sweet-crude.html [Accessed 5 April 2015]

- Schoen J W (12/1/2015) When, and where, oil is too cheap to be profitable CNBC http://www.cnbc.com/id/102326971

- Udland M (11/12/2014) Here is a Simple Way of Seeing Who Gets Screwed Most as Oil Tumbles Business Insider UK http://uk.businessinsider.com/oil-cash-costs-2014-12

- Wikipedia: Unconventional oil http://en.wikipedia.org/wiki/Unconventional_oil#Defining_unconventional_oil

- Reuters (17/2/2014) Global Oil Firms Seen Cutting Exploration Spending Fox Business http://www.foxbusiness.com/industries/2014/02/17/global-oil-firms-seen-cutting-exploration-spending/?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+foxbusiness%2Flatest+%28Internal+-+Latest+News+-+Text%29

- Dancy J (12/11/2013) IEA: The Shale Mirage – Future Crude Oil Supply Crunch? Financial Sense http://www.financialsense.com/contributors/joseph-dancy/iea-shale-mirage-future-crude-oil-supply-crunch (first paragraph of section headed ‘All Liquids Are Not Equal’)

- Yep E (4/11/2014) Falling Prices May Choke Off Energy Flows to Asia The Wall Street Journal http://blogs.wsj.com/moneybeat/2014/11/04/falling-prices-may-choke-off-energy-flows-to-asia/

- Yahoo News (4/3/2015) ExxonMobil cuts spending but predicts higher output http://news.yahoo.com/exxonmobil-cuts-capital-spending-falling-oil-prices-150140256.html

- Yahoo News (3/2/2015) BP cuts investment as sliding oil hits profit https://uk.news.yahoo.com/bp-cuts-investment-sliding-oil-082111522.html#gXQert1

- Macalister T & Monaghan A (29/1/2015) Shell slashes spending and calls for North Sea tax cuts The Guardian http://www.theguardian.com/business/2015/jan/29/shell-cuts-spending-oil-price-slide (see paragraph above Price of Oil chart re Conoco and Occidental