The second of this series of posts focuses on carbon pricing in the UK, on policies for those sectors not currently subject to a carbon price, and on the integration of housing policy with climate change mitigation policy.

The UK has established a carbon price on significant parts of its economy via its Emissions Trading System (ETS), an example of what is sometimes termed a cap-and-trade system. In outline, the government sets an annual cap on the total emissions of firms within the scope of the system and issues emissions permits up to the amount of the cap. Some permits are issued free and some are auctioned, the latter having raised government revenue of just over £4 billion in 2021 (1). Firms within the scope of the scheme must limit their emissions according to the number of permits they have, but trading of permits between firms is allowed and this secondary market determines the carbon price, which is currently around £80 per tonne CO2 equivalent (2). Firms therefore have an incentive to reduce their emissions up to the point at which the marginal abatement cost equals the carbon price.

Such a trading system has the important property of economic efficiency. The carbon price induces firms with lower abatement costs to reduce their emissions by more than those with higher abatement costs. The total reduction in emissions across firms within the scope of the scheme is therefore achieved at least cost.

The fact that some permits are issued free should not limit the effectiveness of the ETS in reducing emissions. Firms which receive free permits still have an incentive to reduce their emissions if they can do so at a cost less than the market price of permits, because they can then sell any unused permits. More fundamentally, the cap applies to all permits, whether auctioned or issued free. The effect of free permits is just distributional: to reduce government revenue while limiting costs to some firms and as a consequence helping to maintain their international competitiveness.

For electricity generation only, the ETS is supplemented by a tax known as Carbon Price Support (CPS) at a current rate of £18 per tonne CO2 equivalent (3).

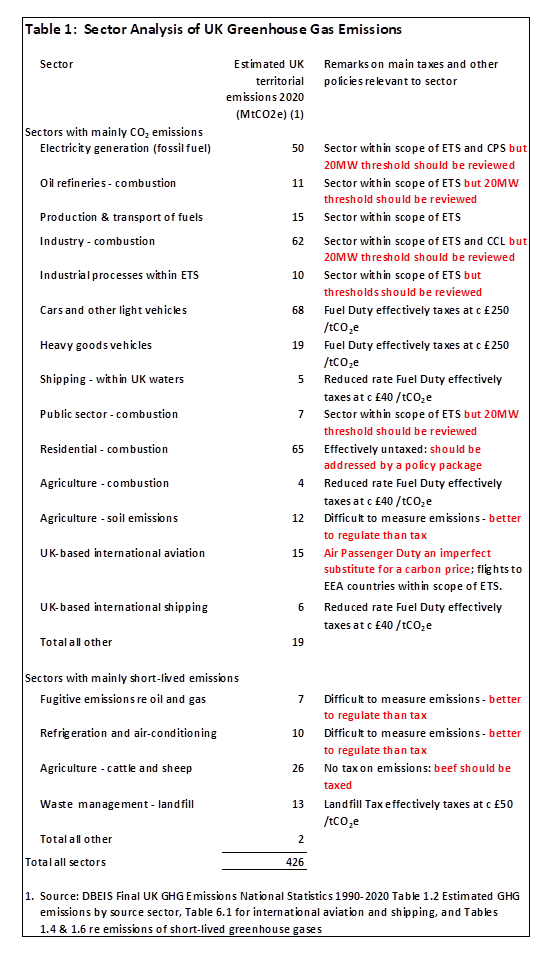

An alternative way to establish a carbon price, advocated by many (4), is via a carbon tax. This has the same efficiency property as a cap-and-trade system. A possible advantage over a trading system is that it could realistically be applied to small firms and individual households, many of which would have difficulty in coping with the complexities of permits and trading. In principle, therefore, a carbon tax could provide a more comprehensive incentive for emissions reduction. To help understand how big an advantage this might be, Table 1 below shows an analysis by sector of UK emissions and indicates which sectors are within the scope of the ETS or taxes providing an incentive to reduce emissions.

Table 1 is simplified in a number of respects, both in the classification of sectors and in the choice of taxes and similar instruments mentioned. Because its data are for 2020, when passenger flights were greatly reduced due to the covid pandemic, the emissions figure for international aviation is much lower than for a normal year. Apart from that, I believe the broad picture it presents is fair. A couple of points merit explanation. For electricity generation (fossil fuel) there is no mention of the significant addition to electricity bills for “environmental and social costs”. The reason for this is that the policy instruments referred to in the third column are only those which provide an incentive for firms to reduce their emissions. It is true that, within these environmental and social costs, a large element relates to climate policy costs, such as obligations under the contracts for difference scheme to subsidise wind and solar power. However, the environmental and social costs are a levy on all electricity bills, not just those for electricity from fossil fuels, so they do not provide any incentive to electricity consumers to choose low-carbon electricity.

The inclusion of Fuel Duty, a tax introduced to raise revenue long before climate change had become an issue, may appear puzzling. Let me offer here the following principle, which I have not seen stated as such, although I think most economists would agree.

People respond to the actual incentives created by a tax in the circumstances in which they find themselves, regardless of the intentions of the authorities in introducing and retaining the tax.

Applied to Fuel Duty which raises the cost of running a petrol-driven car, and given that electric vehicles are now available as an alternative bearing no equivalent tax, the implication is that the duty provides an incentive to decarbonise personal transport. What’s more, the incentive is surprisingly large, as the following calculation shows. The current rate of Fuel Duty on petrol is just over £0.50 per litre, but effectively £0.60 per litre because VAT at 20% is added to the duty (5). When burnt, a litre of petrol yields about 2.4 Kg of CO2 (6). The implicit carbon price is therefore £0.60 / 2.4 or £0.25 per Kg, or £250 per tonne. This is much higher than most estimates of the appropriate current carbon price to optimally address climate change, or the current price of ETS permits. Even for the much lower rates of Fuel Duty applying to fuel for some agricultural uses (marked gas oil or “red diesel”) and shipping (fuel oil) (7), the implicit carbon price is a far from insignificant £40 per tonne.

Let’s now consider the implications of the analysis in Table 1. Of the total estimated emissions of 426 (MtCO2e), 257 are from sectors that are either wholly or mainly within the scope of ETS or subject to Fuel Duty. The main potential benefit from a comprehensive carbon tax is that it could bring carbon pricing to the sectors responsible for the remaining 169 and so provide an incentive for decarbonisation in those sectors. However, of this 169, 58 relates to sectors with mainly short-lived emissions such as methane and hydrofluorocarbons. A carbon tax, understood as a tax on all emissions of greenhouse gases aggregated using the GWP100 metric, is not the most effective way to deal with such emissions. As explained in my previous post, this metric significantly underweights their short-term warming effect. Policy for these sectors should reflect the particular nature of their emissions.

That leaves 111 (MtCO2e) of which the majority (65) relates to the residential combustion sector. This sector consists of the burning of gas and other fuels for domestic heating and cooking (it excludes domestic use of electricity from fossil fuels because in that case the combustion takes place at the power station). I will focus on gas since well over 80% of homes have gas central heating (8). Taxes and levies on gas for domestic use are very low and provide little incentive to users to decarbonise. Gas prices do include an element for environmental and social costs, but these are at a current rate of only about 3%, as compared with about 12% for electricity, including low-carbon electricity (9). There is also VAT at 5%, but that also applies to electricity, again including low-carbon electricity (10). In principle, there is a strong case for establishing a significant carbon price on residential gas use as an incentive to households to reduce their emissions.

At the time of writing, however, the price of gas to households has more than doubled in the last year, largely as a result of changes in global supply and demand. This is one of a number of reasons for what has been termed a “cost of living crisis” in the UK. If the price of gas should in due course fall back to the sort of level seen prior to 2021, then there may be a suitable opportunity to introduce a tax on residential gas use. But to introduce such a tax at the present time would inflict significant hardship on poor households: politically it would be a non-starter.

The conclusion I draw from this review of the main sectors for which no significant carbon price has been established, those outside the scope of both the ETS and Fuel Duty, is that to introduce a comprehensive carbon tax would be far from optimal as a means of mitigating the UK’s contribution to climate change, and – especially in view of its implications for the cost of gas to households – politically infeasible at the present time. Hence:

Proposal 6: Reductions in emissions in those sectors outside the scope of the ETS and Fuel Duty should be sought by suitable sector-specific policies (and not by a comprehensive carbon tax).

A number of sector-specific policies are already in place. For waste disposal, the Landfill Tax, introduced in 1996 and progressively increased in real terms, is a major reason why methane emissions from landfill have fallen from 60MtCO2e in 1990 to 13MtCO2e in 2020 (11). Rather than being the normal means of disposing of waste, landfill is increasingly regarded as a last resort where it is impracticable to use other waste management techniques such as recycling, incineration or generation of biogas.

The use of fluorinated gases including hydrofluorocarbons in refrigeration and air-conditioning has been regulated in the European Union since 2006, and since Brexit equivalent regulations have continued to apply in the UK (12). Regulation is a more suitable instrument than taxation for this sector because emissions are difficult to measure: most occur not during the operation of equipment in good condition, but during manufacture or disposal of equipment, or during operation of poorly maintained equipment. Hence measurement of emissions as a basis for taxation would be difficult, and the more effective approach adopted is regulation to specify which of the many types of these gases are permitted, to limit the total quantity of such gases used, and to promote good practice in manufacture, maintenance and disposal of equipment.

Fugitive emissions arising in the extraction, processing and distribution of oil and gas are difficult to measure for similar reasons. These may be due to leakage at joints or valves, venting and flaring of waste gas, equipment failure and accidents. A variety of regulations and regulatory bodies apply to different parts of the supply chain, with the North Sea Transition Authority (also known as the Oil and Gas Authority), the Environment Agency and the Health and Safety Executive all playing important roles. Despite this, a study in 2021 by CATF, a campaign group, found numerous examples of poor practices resulting in methane emissions (13). This is perhaps unsurprising given that the relevant regulations and regulatory bodies have a variety of objectives of which climate change mitigation is just one. In particular, the North Sea Transition Authority, according to its website:

“… has discretion in the granting of licences to help maximise the economic recovery of the UK’s oil and gas resources, whilst supporting the drive to net zero carbon by 2050” (14)

Hence:

Proposal 7: Regulation and enforcement relating to fugitive emissions from the oil and gas industries should be reviewed to ensure that it gives adequate focus to climate change mitigation and takes due account of the powerful greenhouse effect of methane emissions.

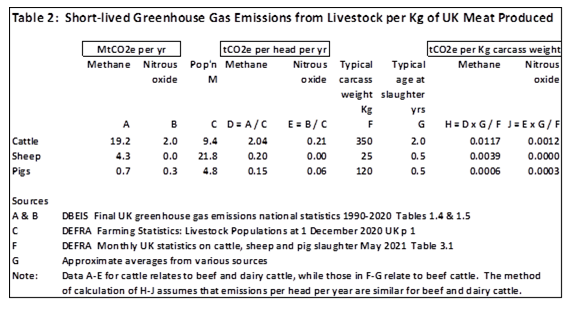

While the raising of livestock is strongly regulated in respect of animal welfare, the UK has no significant policies designed to reduce the methane emissions arising from the digestive process of ruminant animals including cattle and sheep. As Table 1 shows, this is the UK’s largest source of short-lived emissions. Comparing different forms of meat in terms of the methane emissions associated with production of one kilogram of meat, these are highest by far for beef, much lower for lamb, and much lower still for pork and chicken (pigs and chickens not being ruminants) – see Table 2 below. [Added 8 Dec 2024: Table 2 and the conclusions drawn from it contain significant errors. Please see this correction. Proposal 8 below is in need of review, which I hope to undertake in a future post. All other proposals in this post are unaffected. ] This is partly because beef cattle are typically slaughtered at around two years, as against about six months for sheep and pigs. While other greenhouse gases also need to be considered, especially nitrous oxide from livestock waste, the conclusion remains that beef cattle make by far the largest contribution of any livestock to climate change per kilogram of food produced. The contribution of dairy cattle is much less because of the very large quantity of milk that a dairy cow can yield over its lifetime.

Although the amount of a cow’s methane emissions depends on various factors – its breed, diet and age at slaughter – it is significant for all cows (15). Measurement of emissions from a single cattle farm appears impracticable. It is difficult to see how either an emissions tax or regulation could significantly reduce emissions while maintaining beef output. It seems possible that developments in breeding or dietary science will eventually lead to beef production that could genuinely be considered low-methane, and without adverse effects on productivity or animal welfare. For the time being, however, the only practical way to achieve a substantial reduction in emissions is to reduce beef production. Fortunately, many consumers regard beef and other kinds of meat as near substitutes, implying that a small increase in the price of beef would probably lead them to reduce their consumption of beef and increase their consumption of alternatives. This creates an opportunity for a significant contribution to climate change mitigation at the price of a small loss in consumer welfare. Hence:

Proposal 8: The sale of beef should be taxed at a moderate rate with the aim of reducing beef production and so reducing methane emissions from cattle.

Several features of this proposal should be noted. Firstly, while the policy may result in a reduction in total meat production, it is not essential that it should do so. Even if a reduction in beef production were exactly offset by increased production of other meat, a reduction in methane emissions would still result. Secondly, I refrain from making the claim that measures needed for climate change mitigation will, as an additional benefit, promote the adoption of healthier diets. That may be so, but most people I think will want to take advice on diet from experts in that field, rather than as part of an argument about climate change. Thirdly, the policy leaves even those consumers who do not eat pork for religious or cultural reasons with a reasonable choice of other meats: lamb, poultry and – at a somewhat higher price – beef. Fourthly, beef production, especially when the cattle are mainly grass-fed, is land intensive: a reduction in beef production is likely to free some land for other uses. Finally, a tax on the sale of beef will impact not only domestic production but also overseas production of beef for import to the UK, thus making a small contribution to reducing methane emissions abroad and so to Proposal 2 in my previous post.

Policy on emissions from international aviation is constrained by the Chicago Convention and other international agreements which, it is understood, do not allow the taxation of aviation fuel (IATA). As a permitted alternative, in 1994 the UK introduced Air Passenger Duty, a tax per passenger per flight at a rate currently depending on the class of travel and whether or not the distance is more or less than 2,000 nautical miles, with exemption for children under 16 travelling by economy class (16). Since the total tax due in respect of a fllght is therefore roughly correlated with the number of passengers and distance travelled, and since international airliners are mostly fairly similar (given current technology) in their fuel consumption, Air Passenger Duty can be considered a very imperfect substitute for a tax on aviation fuel. In addition, flights to destinations in the European Economic Area are within the scope of the ETS (Airport Watch). The combination of these measures provides little incentive to reduce emissions on long-haul flights, which account for the bulk of emissions (17).

The UK consulted in 2021 on a strategy to decarbonise aviation known as Jet Zero. It includes some sensible ideas on improving fuel efficiency, improving management of airports and airspace, and developing low-carbon aviation fuels. However, none of its scenarios show aviation emissions reducing to zero by 1950 (18). To get to net zero, they all rely on what it terms “abatement outside aviation sector”, that is, technologies yet to be identified for the removal of greenhouse gases from the atmosphere (19). A common feature of all the scenarios is that demand reduction due to carbon pricing is estimated to lead to only a 9% reduction in emissions. That I submit suggests a lack of seriousness about tackling climate change and perhaps a lack of willingness to make the case for discouraging international air travel and reducing the size of the aviation industry.

Having argued above that it would be inappropriate at present to bring residential gas consumption within the scope of carbon pricing, I will not make the same argument for aviation. There is a fundamental difference between the two cases: home heating is an essential while international air travel in most cases is a luxury. Most journeys from UK airports are either for holidays or to visit friends and relatives: less than 20% of journeys in 2019 were for a business purpose (20). To create a stronger incentive to reduce aviation emissions, the practicable and sensible approach in the short term is to increase Air Passenger Duty on long-haul flights. Hence:

Proposal 9: Rates of Air Passenger Duty on long-haul flights should be raised so that the overall structure of rates relates more closely to flight distance and therefore to fuel consumption.

A small – much too small – step in this direction has been taken by the introduction from 1 April 2023 of a slightly higher rate of duty for journeys over 5,500 miles.

Although taxes and levies on gas for domestic use are very low, a number of policies are in place or proposed with the aim of reducing emissions from domestic combustion. The Heat and Buildings Strategy envisages gradual progress towards a future in which buildings are better insulated and heated mainly by electric heat pumps, with heat networks and hydrogen-powered boilers as alternatives in some circumstances (21). Specific policies include:

- The Social Housing Decarbonisation Fund: £800 million for social landlords (local authorities and housing associations) to carry out energy efficiency upgrades (eg insulation) in their tenants’ homes.

- Phasing out the installation of new natural gas boilers from 2035.

- The somewhat misleadingly named Boiler Upgrade Scheme: £450 million offering grants to households to contribute to the cost of installing heat pumps and, in limited circumstances, biomass boilers.

- The Heat Pump Ready Programme: £60 million to support innovation in heat pumps and improve consumer experience in installation.

- In due course, rebalancing energy prices so that heat pumps will be no more expensive to buy and run than gas boilers.

- Ensuring that from 2025 all new homes are ready for net zero so that they will not need to be retro-fitted later.

The Strategy also indicates an ambition of both greatly expanding UK production of heat pumps and reducing their cost, although the specific policies to achieve this are not entirely clear.

The case for promoting the installation of heat pumps on a very large scale in place of gas boilers is twofold. Firstly, heat pumps are powered by electricity, so are a zero-carbon source of heating provided the electricity is itself from a zero-carbon source. Secondly, they are an extremely efficient source of heat. For other forms of heating such as gas boilers and conventional electric heaters, efficiency, measured as the ratio of heat energy output to energy input, cannot exceed 100%. A heat pump, however, because it uses electricity to draw in heat from the air or ground outside a building, can achieve efficiency of 400% or more (22). Additional benefits are that heat pumps, once installed, require little maintenance, and some models have the facility, when needed, to go into reverse and act as air-conditioners, a consideration that may became increasingly important as we need to adapt to climate change.

However, heat pumps also have disadvantages. The initial cost of purchase and installation depends on circumstances, but can easily be more than £10,000 (23), as against typically £2,000 to £3,000 for a gas boiler. Costs may fall somewhat in future as an expansion of heat pump manufacturing in the UK yields economies of scale. But it would be over-optimistic to expect a dramatic fall in costs such as solar power has experienced over the last decade. The unfamiliarity of heat pumps to many people in the UK may suggest that they are a relatively new technology with plenty of scope both for improvement and cost reduction. In fact, the first heat pump was built in 1856 (24). In the UK in 1945, an engineer named John Sumner developed a large-scale heat pump to heat the premises of the Norwich City Council Electrical Department, and later installed a heat pump in his own home. Subsequently, the technology was adopted in some other countries much more widely than in the UK: the US is estimated to have had 750,000 heat pumps in operation by 2008. By 2020, almost 180 million heat pumps were in use worldwide, the majority having been installed in new buildings (25). Considerable numbers were in countries colder than the UK, including Norway, Sweden and Finland. Two conclusions should be drawn from this. One is that there has already been plenty of opportunity across the world for innovation to improve the performance of heat pumps and reduce costs, suggesting that the benefits of further innovation may be only marginal. The idea that heat pumps will eventually be no more expensive than gas boilers appears rather optimistic. The other is that there is a lot of experience worldwide of installing heat pumps in different circumstances, and the UK should be drawing on that experience as much as possible (an example of Proposal 4 in my previous post).

To heat a home of any size, a heat pump alone is insufficient. The heat pump itself simply draws in heat from outside, but that heat then needs to be distributed to all parts of the home. A variety of systems are in use, but to illustrate some potential complications I will refer to what is termed an air-to-water heat pump (26). In outline, an outdoor unit takes in heat from the air and transfers it via a heat exchanger to a hot water tank. Hot water is then circulated via a network of pipes to radiators located in the rooms of the home. Suppose now that such a system is to be installed in a home which previously used a gas-powered central heating system. The conversion might seem fairly straightforward: the pipe network and radiators can be retained, the hot water tank can go in the space previously occupied by the boiler and, assuming the boiler was next to an external wall (as is likely for release of its waste gases) the outdoor unit can be fitted on the external side of the wall.

In practice, however, there can be various difficulties which will make the installtion of a heat pump system more complicated, more costly, and perhaps impossible. In some homes, especially flats, the boiler is not on the ground floor. It may then be possible to fit an outdoor unit outside an upper floor, but it will need suitable physical support, and in a block of flats will probably require the landlord’s permission which could be refused, if only to preserve the external appearance of a block. Even if the boiler is on the ground floor, the ground outside the wall may not be a suitable place to locate an outside unit. In my home, for example, the boiler is next to an external wall, on the other side of which is a public pavement: an outside unit would have to go somewhere else, requiring fitting additional pipework to connect to the existing network with disruption to another ground floor room. A further complication is that the existing radiators may not be suitable: a heat pump system will not heat water to as high a temperature as a gas boiler, and therefore larger radiators may be needed to yield the same heating effect (27). Fitting larger radiators may in turn require changes to the location of furniture, and make it difficult to fit, say, a bed and a wardrobe into a small bedroom. This helps to explain why some heat pump systems avoid radiators and instead use underfloor heating, but that further adds to the installation cost.

The conclusion to be drawn is that, although heat pump systems are an excellent option when included from the outset in designs for new homes, retro-fitting them into existing homes is in many circumstances awkward and expensive, and in some cases practically impossible. It would not be surprising if some home-owners are induced by unscrupulous or poorly-trained salesmen in conjunction with government financial help to accept the installation of systems which turn out to be less satisfactory than their previous gas central heating.

A further feature of heat pump systems – although it may seem counterintuitive – is that they require coolants, typically hydrofluorocarbons or similar chemicals (28). That means that, just as explained above for refrigerators and air-conditioners, heat pump systems may contribute to the atmospheric concentration of short-lived greenhouse gases. Hence:

Proposal 10: The government’s aims of encouraging the installation of heat pump systems and reducing their cost should not be at the price of weakening measures to limit emissions of fluorinated gases.

The essential problem with the Boiler Upgrade Scheme is that it is not technology-neutral. The government has picked its winners – heat pumps and, in limited circumstances, biomass boilers – and other low-carbon heating technologies do not qualify for financial support. Why should equivalent financial support not be available for a household which replaces a gas-powered central heating system with modern electric heaters and also improves its insulation? Provided the electricity is from a low-carbon source, such a system is just as low-carbon as a heat pump system, and has the advantage of avoiding any risk from fluorinated gases. If storage heaters are used it can also contribute to balancing the timing of supply and demand for electricity – of which more in another post. For the household, the capital cost may be much lower than for a heat pump system, and installation much less disruptive. Hence:

Proposal 11: Eligibility for the Boiler Upgrade Scheme should be extended to any household conversions from fossil-fuel heating systems to electric or other low-carbon heating systems, subject to defined standards of loft and wall insulation and glazing so as to limit energy consumption for heating.

Other low-carbon systems would include those powered by hydrogen (if and when hydrogen replaces natural gas in the local or national gas grid) and by solar thermal. The Heat and Buildings Strategy notes the possible potential of hydrogen as a heating fuel which does not produce CO2 emissions because its combustion yields water vapour only (29). Provided hydrogen can be produced in a zero-carbon way and distributed safely, it appears to offer an attractive heating solution for homes currently heated by gas central heating which for whatever reason are unsuitable for a heat pump, with only the boiler needing to be replaced while pipework and radiators could remain. However, experience worldwide with hydrogen as a home heating fuel is very limited (30), and the Heat and Buildings Strategy sensibly plans safety and feasibility testing leading to a “village scale” trial by 2025 (31).

Some other aspects of the Heat and Buildings Strategy are also questionable. The date of 2035 for phasing out the installation of new natural gas boilers is explained in the Strategy as being 15 years before 2050, around 15 years being the lifetime of such a boiler (32). That is presumably just an average: some will last longer and, if installed just before 2035, may continue, if permitted, to contribute to carbon emissions beyond 2050. Furthermore, even if every gas boiler lasted exactly 15 years, many boilers might be contributing to carbon emissions right up to 2049, which would be consistent with the 2050 target but hard to reconcile with the plan of steadily reducing carbon budgets over the whole period to 2050. Also, the “phasing out” wording leaves it unclear what exactly the government intends, and seems to represent a retreat from earlier statements referring to a “ban” which prompted strong reactions in some quarters. There is clearly a dilemma for the government in trying to promote the installation of heat pumps and development of the heat pump industry to that end while avoiding the opposition that could be generated by perceptions of high costs for households and (even if some years away) compulsion. Its hope, presumably, is that potential opposition can be overcome by a combination of innovation leading to cost reductions, support for improvements in consumer experience, financial support for early adopters, and a rebalancing of prices between electricity and gas. Whether that approach will be successful appears far from certain. Hence:

Proposal 12: Progress in phasing out the use of fossil fuels for home heating should be carefully monitored, and consideration given to a ban on new fossil-fuel systems (in addition to financial support for alternatives) should progress be insufficient.

It might be asked why it should be required that all new homes from 2025 be net zero ready. Clearly, it is much cheaper to install zero-carbon heating when a home is built than to install a conventional heating system and then retro-fit later. But is that a sufficient reason to ban anyone from building or buying a new home that has, say, gas central heating, at a time when such heating is still widely used in older homes? Why not rely on the good sense of buyers to understand that, given the broad direction of climate change policy, buying a home that will need to be retro-fitted later represents a poor long-term investment unless the price is at an appropriate discount relative to a net-zero-ready but otherwise similar home, and on the recognition by developers that they will not make profits by selling new homes at such a discounted price? One reason is that buyers may be unaware of the need for subsequent retro-fitting, or have no clear idea of how much it might cost or how much disruption it might involve. But even if they are well-informed on these points, the need for retro-fitting may have little salience for them relative to other points they have to consider when choosing a new home, such as number of bedrooms, location, transport links, and local facilities. It seems quite possible, therefore, that in the absence of government intervention, developers would still find a profitable market for new homes that were not net zero ready.

There is a further reason for government intervention which also illustrates a more general point about the political economy of climate change. I referred above to the broad direction of climate change policy as a “given”. But it isn’t a given: whether policies designed to progressively reduce emissions leading to net zero by 2050 will receive sufficient political support to enable them to be delivered is far from certain (33). Even if bringing climate change to a halt is in the long-term interests of all, and even if many people are willing to accept some degree of sacrifice to that end, there are bound to be groups seeking to oppose particular climate change policies which would adversely affect their interests in the short and medium term. Effective government in respect of climate change mitigation is not only about adopting the ‘right’ policies: it is also about building support for those policies by strengthening supportive interest groups and weakening opposition (34). The large number of households with gas central heating is a substantial interest group, and I have already noted above that to put a significant carbon price on domestic gas use in current circumstances would be a political non-starter. Financial support for the installation of heat pumps is one policy which will tend to weaken that interest group, by reducing its numbers. Requiring new homes to be net zero ready may not reduce by very much the absolute number of households with gas heating: probably most new homes will be a net addition to the housing stock, rather than replacing existing homes. It will however increase the proportion of homes that are net zero ready, and so gradually weaken potential opposition to measures that are likely to be needed eventually such as a carbon price on domestic gas and a ban on new gas heating installations.

The impact of the requirement will depend on how many new homes are built. Average annual UK housing completions over the five pre-pandemic years 2015-19 were about 190,000 (35). At that rate, completions during the whole period 2025-49 would be just under 5 million, about one-sixth of the current total housing stock of 29.5 million (36). The impact would be much larger if annual completions were to increase to 300,000, a target indicated in the 2019 Conservative manifesto (37).

A faster rate of homebuilding would have two significant advantages in respect of climate change mitigation, over and above the general economic advantages of lowering housing costs by increasing supply and of facilitating labour mobility. One would be to increase more rapidly the net zero ready proportion of the total housing stock. The other would be, by increasing overall housing supply, to lower housing costs and so increase the proportions of household incomes available for other expenditure. This in turn would increase the willingness of households to bear the costs needed to address climate change. Putting the point another way, it is likely to be difficult to secure political acceptance for extra costs on households to reduce the UK’s emissions, let alone to provide generous financial help for poor countries in respect of climate change, while many households have little choice but to spend a large proportion of their incomes on housing, leaving them in the position of just managing – or not managing – in respect of other essentials such as food and fuel.

The rate of homebuilding could be increased with minimal public expenditure, simply by relaxing planning restrictions which can make it difficult for developers to obtain approval for new housing in areas where people want to live. It is unfortunate that the government appears to have abandoned the main thrust of its White Paper Planning for the Future (2020), considered in this post, which included a proposal to designate growth areas within which outline approval for suitable housing development would be automatically secured. It is also unfortunate that, despite the current intense concern and interest regarding the cost of living crisis, the cost of housing seems to be the elephant in the room, rarely mentioned despite being for many households by far the largest element in their spending.

It has to be acknowledged that there is currently a substantial carbon footprint associated with the building of a new home, arising mainly in the manufacture of materials such as bricks, tiles, glass and cement. The quantity, sometimes termed the embodied carbon, depends on the type of home and materials used, but for an average house is of the order of 60 tonnes CO2 equivalent (38). To put that figure into perspective, annual emissions from an average house heated by gas central heating are about 2.4 tonnes. We can infer that, in a scenario where an average gas-heated house is replaced by a new zero-carbon house, the ‘carbon payback period’, that is, the period it takes for the embodied carbon to be offset by the avoidance of ongoing emissions from gas heating, is 25 years (60 / 2.4). The conclusion to be drawn is that, considered purely as a means of climate change mitigation, and even before consideration of cost, replacing old homes with new is a rather poor approach.

Unfortunately, current VAT rules tend to favour new buildng over renovation. VAT is not chargeable on the construction of new homes. Under rules introduced in the April 2022 Budget, VAT is also not chargeable in most circumstances on the installation of energy-saving materials including heat pumps, insulation and solar panels. However, there is no general VAT exemption for home repairs and refurbishments. If therefore a home is in very poor condition but capable of being refurbished to a good standard, the extra VAT cost could tip the balance in favour of demolition and rebuilding, despite the much larger embodied carbon that would result.

Most demand for new homes is for reasons unrelated to climate change mitigation, including population growth, employment opportunities in particular regions, and (perhaps becoming increasingly significant in future) adaptation to climate change via replacement of homes lost or uninhabitable due to sea level rise, coastal erosion or frequent flood risk. In such cases the carbon payback period is less relevant, but the issue of embodied carbon remains. Indeed, those keen to maintain current planning restrictions might deploy the argument that such restrictions contribute to climate change mitigation. However, such restrictions are not the best way to address the carbon footprint of building new homes.

Like all greenhouse gas emissions, the embodied carbon associated with new homes is a form of market failure, a negative externality consisting in the fact that, without government intervention, developers and home buyers do not bear the cost of the damage the emissions cause. There are three reasons why is it better to address that externality via a carbon price on building materials than by stringent planning restrictions with the effect of limiting the number of homes built. Firstly, a carbon price on building materials at the same rate as on other goods within the scope of the ETS will enable the market to find the best trade-off between building new homes and producing other goods, subject to the ETS cap on emissions. More formally, it will ensure that profit-maximising developers build homes up to the point at which the marginal benefit per unit of emission from new homes equals that from other goods, assuming that benefit is reflected in the prices buyers are willing to pay. Current planning restrictions, by contrast, yield a rate of homebuilding that depends on the vagaries of separate decisions by local planning authorities having little regard either to national housing needs or to climate change mitigation. Secondly, the carbon price on materials is location-neutral: unlike planning restrictions, it has no bearing on developers choice of where to build new homes. Other things being equal, therefore, it enables developers to choose to build homes in areas where people want to live. Thirdly, the carbon price provides an incentive to design new homes, in terms of size and choice of materials, with less embodied carbon. Strategies for limiting embodied carbon include avoiding sites requiring deep foundations, choosing simple, compact shapes (eg rectangles rather than L-shapes), and using timber-framed structures where possible.

Summarising the above, I propose the following package of measures to integrate housing development policy and climate change mitigation policy:

Proposal 13: To facilitate an appropriate trade-off between the economic benefits of housing development and the need to mitigate climate change:

- Planning restrictions on housing development should be relaxed, broadly along the lines of the White Paper Planning for the Future (2020);

- All new homes put on sale from 1 January 2023 should be required to be net zero ready;

- Repair and refurbishment of existing homes, including installation of insulation and low-carbon heating systems, should have the same VAT status as construction of new homes;

- The manufacture of materials used in building new homes and associated infrastructure should be subject to a carbon price at a rate consistent with the UK’s carbon budget at the time.

All these points require changes from current policy, although the changes needed are largest for (a) and (c). Point (b) implies bringing forward to 2023 the date of 2025 specified in the Heat and Buildings Strategy. There is no justification for allowing homes that will need retro-fitting to be sold for a further two years.

Point (d) is largely implicit in the ETS, which applies to the large-scale manufacture of, among other materials, bricks, tiles, cement, glass, metals and plaster board (39). However, the scope of the ETS in many sectors is limited by thresholds. Where production involves fuel combustion, the threshold is often 20 MW. Other sectors have thresholds in terms of daily production capacity, including bricks and tiles (75 tonnes), glass (20 tonnes), and cement clinker (500 tonnes if from rotary kilns, 50 tonnes if from other furnaces). Hence:

Proposal 14: The various sector thresholds set out in Schedule 2 of The Greenhouse Gas Emissions Trading Scheme Order 2020 should be reviewed to ensure that they are no higher than necessary.

A threshold might be considered necessary if, for production at any scale below the threshold, the costs of compliance and enforcement, including measurement of emissions, would be disproportionate to any benefit from abatement of emissions. The logic behind the various current thresholds is far from clear; one suspects that they were arrived at partly as a result of lobbying by firms or industry bodies. What’s more, the threshold quantities are quite large. The power rating of a central heating boiler for an average house might be about 30 kW (40). The 20 MW threshold is therefore equivalent to about 670 (20 x 1,000 / 30) such boilers. For cement clinker, the daily 500 tonnes threshold is equivalent to about 180,000 tonnes annually, which is about 2% of total annual cement production (9 M tonnes (41 Statista)). Because of these thresholds, some of the embodied carbon in new homes, and more generally much small and medium scale industrial production, is not currently subject to a carbon price.

Notes and References

- ICAP Factsheet 99 – United Kingdom https://icapcarbonaction.com/system/files/ets_pdfs/icap-etsmap-factsheet-99.pdf p 3

- EMBER Carbon Prices https://ember-climate.org/data/data-tools/carbon-price-viewer/

- HM Treasury Spring Statement 2022 – Policy Costings https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1062462/Policy_Costings_Document_Spring_Statement_2022.pdf p 31

- Economists’ Statement on Carbon Dividends Organized by the Climate Leadership Council https://www.econstatement.org/

- HM Government Tax on Shopping and Services – Fuel Duty https://www.gov.uk/tax-on-shopping/fuel-duty

- Carbon Independent https://www.carbonindependent.org/17.html#:~:text=The%20CO2%20emissions%20from%20petrol,1%20gallon%20is%204.546%20litres).

- HM Government (17 May 2022) Excise Duty hydrocarbon fuel rates https://www.gov.uk/government/publications/rates-and-allowances-excise-duty-hydrocarbon-oils/excise-duty-hydrocarbon-oils-rates

- English Housing Survey: Energy Report 2019-20 https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1055629/Energy_Report_2019-20.pdf p 18

- Ralston J, ECIU (2022) Energy bills: getting the balance right https://eciu.net/insights/2021/rebalancing-energy-bills-and-carbon-prices-what-are-the-options

- SSE Energy Services Costs that make up your gas and electricity bills https://sse.co.uk/help/energy/gas-electricity-bill-payment/bill-price-breakdown

- DBEIS Final UK greenhouse gas emissions national statistics 1990-2020 https://www.gov.uk/government/statistics/final-uk-greenhouse-gas-emissions-national-statistics-1990-to-2020 Table 1.4 Row 75

- The Fluorinated Greenhouse Gases (Amendment) (EU Exit) Regulations 2021 (SI 2021/543) https://www.legislation.gov.uk/uksi/2021/543/contents/made

- Clean Air Task Force (2021) New evidence of UK methane pollution uncovered ahead of COP26 https://www.catf.us/2021/10/uk-methane-pollution-uncovered/#038;swpmtxnonce=4b770f2d2f

- North Sea Transition Authority – Licensing & consents – Overview https://www.nstauthority.co.uk/licensing-consents/overview/

- Dewhurst R & Miller G (2019) How do different livestock types, sizes and breeds differ in their greenhouse gas emissions? pp 3-4 https://www.climatexchange.org.uk/media/3651/how-do-different-livestock-types-sizes-and-breeds-differ-in-their-greenhouse-gas-emissions.pdf

- H M Revenue & Customs Rates for Air Passenger Duty https://www.gov.uk/guidance/rates-and-allowances-for-air-passenger-duty

- Dept for Transport (2021) Jet Zero Consultation para 3.14 p 26 https://www.gov.uk/government/consultations/achieving-net-zero-aviation-by-2050

- Dept for Transport, as (17) above pp 13-15

- Dept for Transport, as (17) above pp 35-36

- Statista Purpose of air travel at airports in the United Kingdom 2002-2019 https://www.statista.com/statistics/303774/travel-purpose-trends-at-uk-airports/#:~:text=This%20general%20UK%20trend%20shows,to%2017%20percent%20in%202019.

- DBEIS (2021) Heat and Buildings Strategy https://www.gov.uk/government/publications/heat-and-buildings-strategy

- Pears A & Andrews G (2016) Back to Basics: Heat Pumps https://www.eec.org.au/for-energy-users/technologies-2/heat-pumps

- EDF Energy A complete guide to air source heat pumps https://www.edfenergy.com/heating/advice/air-source-heat-pump-guide

- Finn-Geotherm The History of Heat Pump Technology https://finn-geotherm.co.uk/the-history-of-heat-pumps/

- International Energy Agency Heat Pumps https://www.iea.org/reports/heat-pumps

- Idronics Air-to-water heat pump configurations https://idronics.caleffi.com/article/air-water-heat-pump-configurations

- Kensa Heat Pumps – Radiators https://www.kensaheatpumps.com/how-do-heat-pump-systems-work/#:~:text=Radiators%20should%20be%20oversized%20to,efficiency%20of%20the%20heating%20system.

- WSP (2018) The importance of refrugerants in heat pump selection https://www.wsp.com/en-GB/insights/the-importance-of-refrigerants-in-heat-pump-selection

- DBEIS, as (21) above p 82

- International Energy Agency (2021) Hydrogen https://www.iea.org/reports/hydrogen

- DBEIS, as (21) above p 233

- DBEIS, as (21) above p 20

- Lockwood M (2013) The political sustainability of climate policy: the case of the UK Climate Change Act Global Environmental Change 23 (2013) pp 1339-40 https://core.ac.uk/download/pdf/82754883.pdf

- Lockwood M, as (33) above pp 1340-41

- Statista New homes completed … in the UK from 1949 to 2019 https://www.statista.com/statistics/746101/completion-of-new-dwellings-uk/

- ONS Dwelling stock by tenure, UK, 2020 edition Table 1 row 25 https://www.ons.gov.uk/peoplepopulationandcommunity/housing/datasets/dwellingstockbytenureuk

- Conservative Party Manifesto 2019 p 31 https://www.conservatives.com/our-plan/conservative-party-manifesto-2019

- Barrett J & Wiedmann T (2007) A Comparative Carbon Footprint Analysis of On-Site Construction and an Off-Site Manufactured House p 9 http://www.carbonconstruct.com/pdf/comparative_carbon_footprint_analysis.pdf

- HM Government The Greenhouse Gas Emissions Trading Scheme Order 2020 Sch 2 Table C https://www.legislation.gov.uk/uksi/2020/1265/schedule/2/made

- PlumbNation (2021) What size boiler do I need for my home? https://www.plumbnation.co.uk/blog/what-size-boiler-do-i-need-for-my-home/

- Statista Cement production volume in Great Britain from 2001 to 2019 https://www.statista.com/statistics/472849/annual-cement-production-great-britain/#:~:text=In%202019%2C%20plants%20in%20Great,levels%20seen%20prior%20to%202009.